Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

After more than a decade of ultra-low interest rates, higher interest rates have been a tough adjustment. But as with all change, it may help to step back for some perspective. These “high” interest rates are, in a sense, a return to normalcy: Interest rates above 4% were actually quite common prior to 2008.

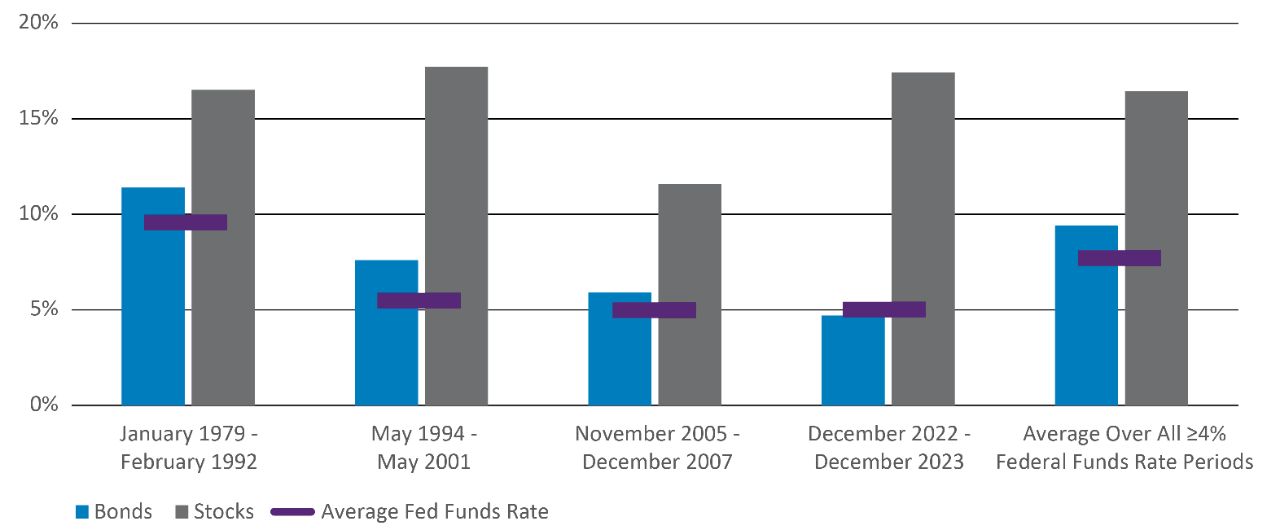

And historically, these higher interest rates were helpful for investors: Stocks and bonds have generated solidly positive returns in previous periods in which interest rates were above 4%.

Markets Have Performed Well When Rates Were At or Above 4%

Average Annualized Returns (%)

Chart data: 1979–2023. Past performance does not guarantee future results. Investors cannot directly invest in indices. Bonds represented by the Bloomberg US Aggregate Bond Index. Stocks represented by the S&P 500 Index. Rates represented by the federal funds rate, the target interest-rate range set by the Federal Open Market Committee. Data Sources: Morningstar and FRED, 2/24.

Fed Speak? Greek to Me

The federal funds rate is the rate at which banks borrow from each other overnight. This influences the rates on everything from mortgages to the interest you earn on CDs or a savings account. A higher federal funds rate can benefit savers but make life more difficult for borrowers.

The Federal Reserve’s (Fed) Federal Open Market Committee sets the federal funds rate and can lower it to encourage borrowing and boost the economy, like it did for an extended time after the Global Financial Crisis. That period of near-zero rates lasted so long it felt normal, but it was actually quite unusual: With the exception of the 2008-2022 time frame, rates have only been below 1% for only a handful of months since 1954.

Conversely, the Fed can raise rates to help tame inflation, discourage borrowing, and slow an overheating economy—which is why rates rose so rapidly after the COVID-19 pandemic. This created a challenging environment for investors, as both stocks and bonds performed poorly when rates rose dramatically.

Adapting to the Not-So-New Normal

The encouraging news is that the shock of rising rates should be behind us. Fed officials have said they’re willing to be patient and move slowly to lower rates, which is a sign they see continued strength in the overall economy going forward. And with a history of strong performance during previous periods of higher rates, waiting for a “better” time to invest could mean missed opportunities for both stock and bond investors.

Talk to your financial professional to make sure you’re invested in the appropriate mix of investments for today’s interest-rate environment.

Bloomberg US Aggregate Bond Index is composed of securities from the Bloomberg Government/Credit Bond Index, Mortgage-Backed Securities Index, Asset-Backed Securities Index, and Commercial Mortgage-Backed Securities Index.

S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

Important Risks: Investing involves risk, including the possible loss of principal. • Fixed income security risks include credit, liquidity, call, duration, and interest-rate risk. As interest rates rise, bond prices generally fall.