“Boy, that escalated quickly!” While we don’t want to trivialize the war in the Middle East or the market sell‑off since February, this memorable line uttered by Will Ferrell in “Anchorman” is one cheeky way to describe the about‑face in market returns and risk appetite relative to January’s optimistic outlook. It’s also a reminder that quick turns in expectations can amplify moves as investors scramble to cover wrong‑footed positions in equities and bonds.

While technical factors have certainly played a role in the dramatic moves to date, we think the conflict warrants a reset of expectations for risk and returns this year. The reason: With some energy infrastructure already damaged and the potential for more, energy supply-chain disruptions and elevated oil and gas prices could persist for months, even if the Strait of Hormuz reopens fully during the ceasefire. Of course, it’s worth emphasizing that the situation remains fluid and subject to change in the coming days and weeks.

The macro backdrop is stagflationary, with potential implications across asset classes. Higher energy prices are feeding into headline inflation (including food, due to higher fertilizer prices), while also adding about one percentage point to core inflation as they spill over into transportation, chemicals, packaging, pharmaceuticals, and all things plastic. Depending on how long elevated oil prices persist, we also think growth expectations could be dented as consumers cut back. Companies’ decisions about whether to absorb higher input costs or pass them through to customers will be key for earnings expectations and, by extension, the labor market.

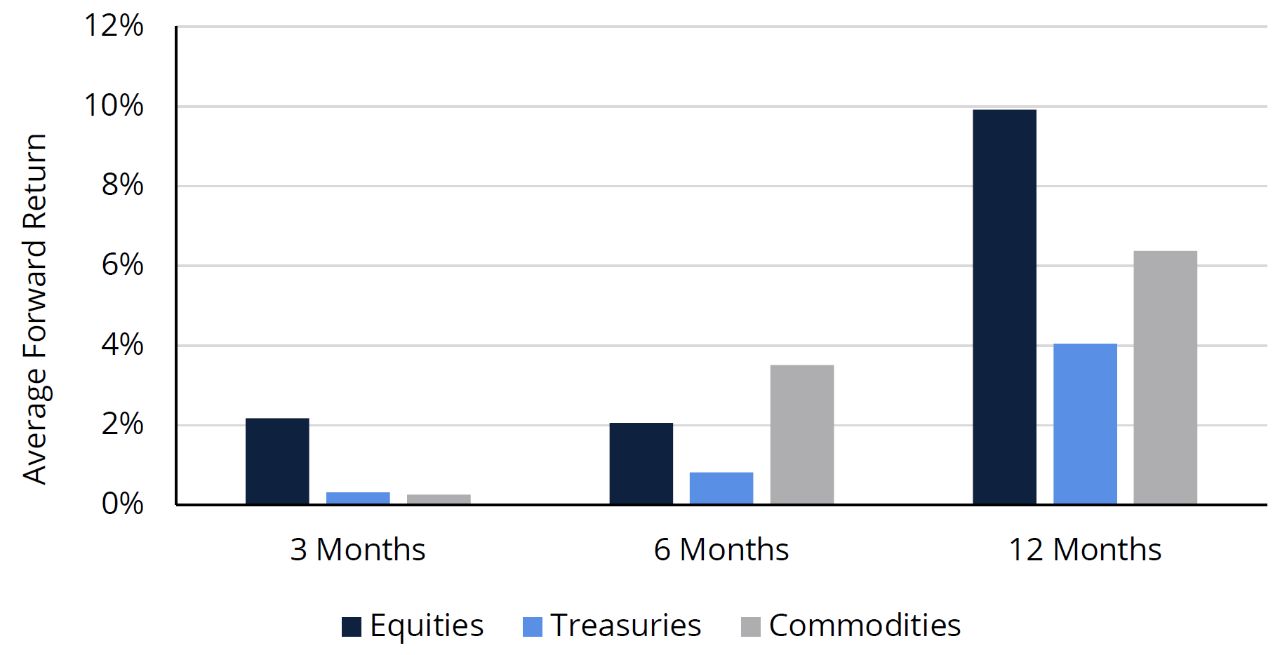

Despite these headwinds, we maintain our moderately overweight view on global equities over our 12‑month horizon for several reasons. The year began with strong earnings momentum, the AI innovation theme remains intact, valuations are more attractive, and fiscal policy remains supportive. In addition, elevated volatility and differences in sensitivity to energy prices have created regional opportunities within equities. Finally, in past stagflationary periods marked by oil price spikes of at least 20%, markets have posted decent returns within 12 months (FIGURE 1). We favor the US and EMs and hold a moderately underweight view on Europe ex‑UK and an underweight view on the UK.