Our Multi-Asset Views

| Asset Class | View | Change |

| Global equities | Moderately OW | — |

| DM govt. bonds | Moderately OW | 🡅 |

| Credit spreads | Moderately OW | — |

| Commodities | Moderately OW | 🡅 |

| Cash | Underweight | 🡇 |

| Within Asset Classes | ||

| Global Equities | ||

| US | Neutral | 🡇 |

| Europe | Neutral | — |

| Japan | Neutral | 🡇 |

| China | Neutral | 🡅 |

| EM ex China | Neutral | 🡅 |

| DM Government Bonds | ||

| US government | Neutral | 🡅 |

| Europe government | Neutral | 🡇 |

| Japan government | Neutral | — |

| Credit Spreads | ||

| US high yield | Neutral | 🡅 |

| Europe high yield | Moderately OW | — |

| Global IG | Neutral | 🡇 |

| EMD | Moderately UW | 🡇 |

| Bank loans | Neutral | — |

| Securitized assets | Moderately OW | 🡅 |

OW = overweight, UW = underweight

Views have a 6-12 month horizon and are those of the authors and Wellington’s Investment Strategy Team. Views are as of 6/30/24, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients. This material is not intended to constitute investment advice or an offer to sell, or the solicitation of an offer to purchase shares or other securities.

Confident in the positive fundamental backdrop, we’ve maintained our moderately overweight view on global equities but no longer have a regional preference. We’ve raised our view on emerging-market (EM) equities to neutral: valuations are relatively inexpensive but politics and the delay in Fed rate cuts are weighing on the macro outlook. Within risk assets, we also favor high-yield credit, given the macro backdrop and the role that lower US yields have played in improving access to liquidity. We have a slight preference for European high yield given wider spreads in reaction to French political concerns. Within commodities, we have a moderately overweight view on oil given OPEC’s desire to keep the market tight and oil futures’ positive carry.

Turning to government bonds, slowing growth, declining inflation, and eventual central-bank easing underpin our moderately long-duration stance across developed-market (DM) regions. This view is challenged somewhat in Japan, where the Bank of Japan (BOJ) seems out of sync with inflation data, especially as the yen sinks to new lows, but we think the central bank could remain patient given weaker growth data.

Equities: Still Positive, But Broader Would Be Better

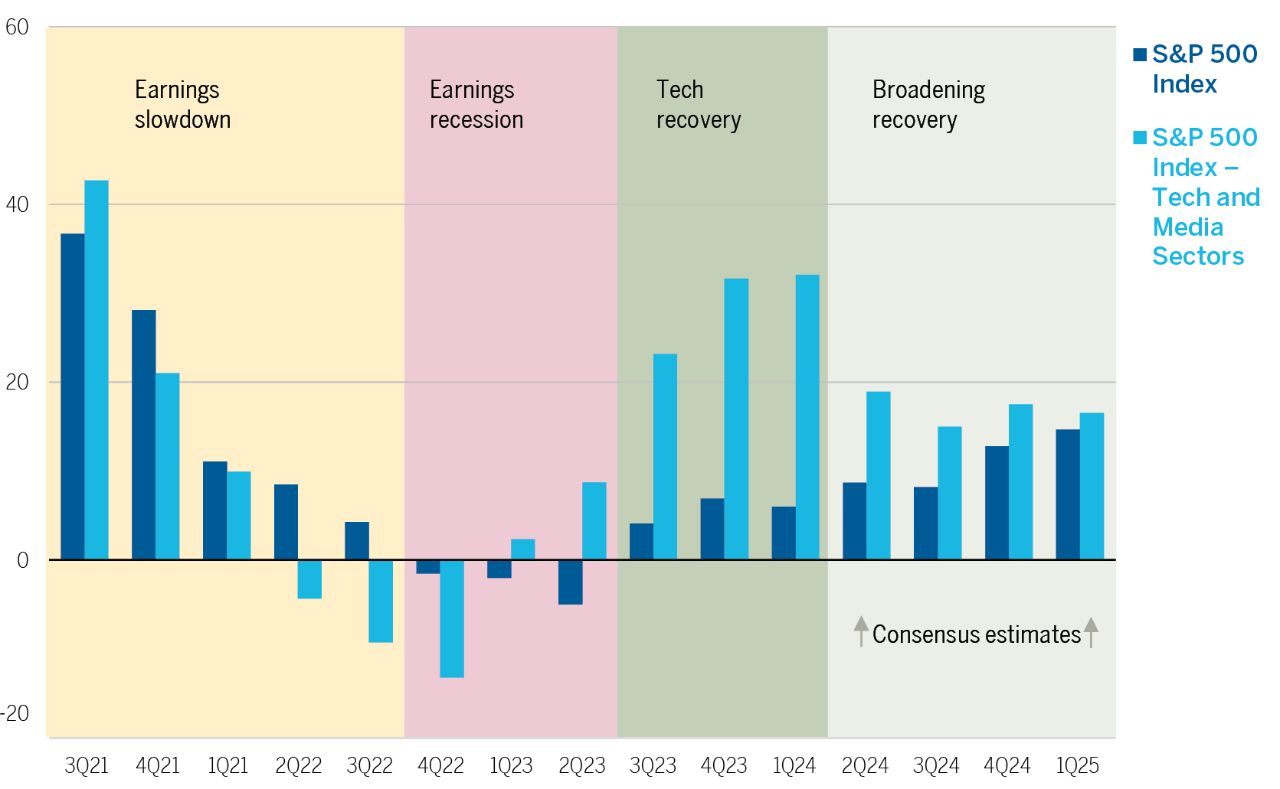

We maintain a moderately overweight view on global equities. While economic growth momentum has slowed in the US, global activity continues to improve, and the rate outlook in major markets is more realistic. Meanwhile, global earnings revisions continue to inflect positively, and we expect earnings growth, rather than valuation expansion, to drive returns over the next 12 months. We also expect earnings growth to be more broad-based than it has been in the narrow market driven by mega-cap tech stocks.

On the negative side, the resumption of mega-cap outperformance and the narrowing market advance in the latter half of the second quarter is a source of concern. The recent softness in growth data in the US and the flare-up in eurozone political risk have probably compounded market concentration dynamics. We would likely turn more positive on global equities if we saw signs that the equity rally was broadening out or if valuations cheapened in response to political flare ups or weaker economic data.

We‘ve reduced our view on Japan to neutral. We first moved to an overweight view on the country in November 2022, based on strong evidence of a macro regime shift and improvements in corporate governance. The push for better corporate governance, returns to activism, and rising margins have been helpful, and our view is that Japanese equities could continue to re-rate over the medium term and reduce the margin/return-on-equity gap vs. other markets.

However, we’re less bullish on macro conditions in the short term. Our outlook on inflation and rates is above consensus, and we believe the BOJ is behind the curve on policy settings and risks losing credibility. While the BOJ has (seemingly) intervened as yen depreciation has intensified, this has provided only temporary support, and more monetary-policy action will likely be needed to stabilize the currency. All of this raises the potential for higher macro volatility or uncertainty in the short term, which means the overall risk/reward skew is less positive than a few months ago. The caveat to this view is that Japanese equities’ relative performance has become less tied to moves in the yen as companies have increasingly diversified their production abroad through subsidiaries.

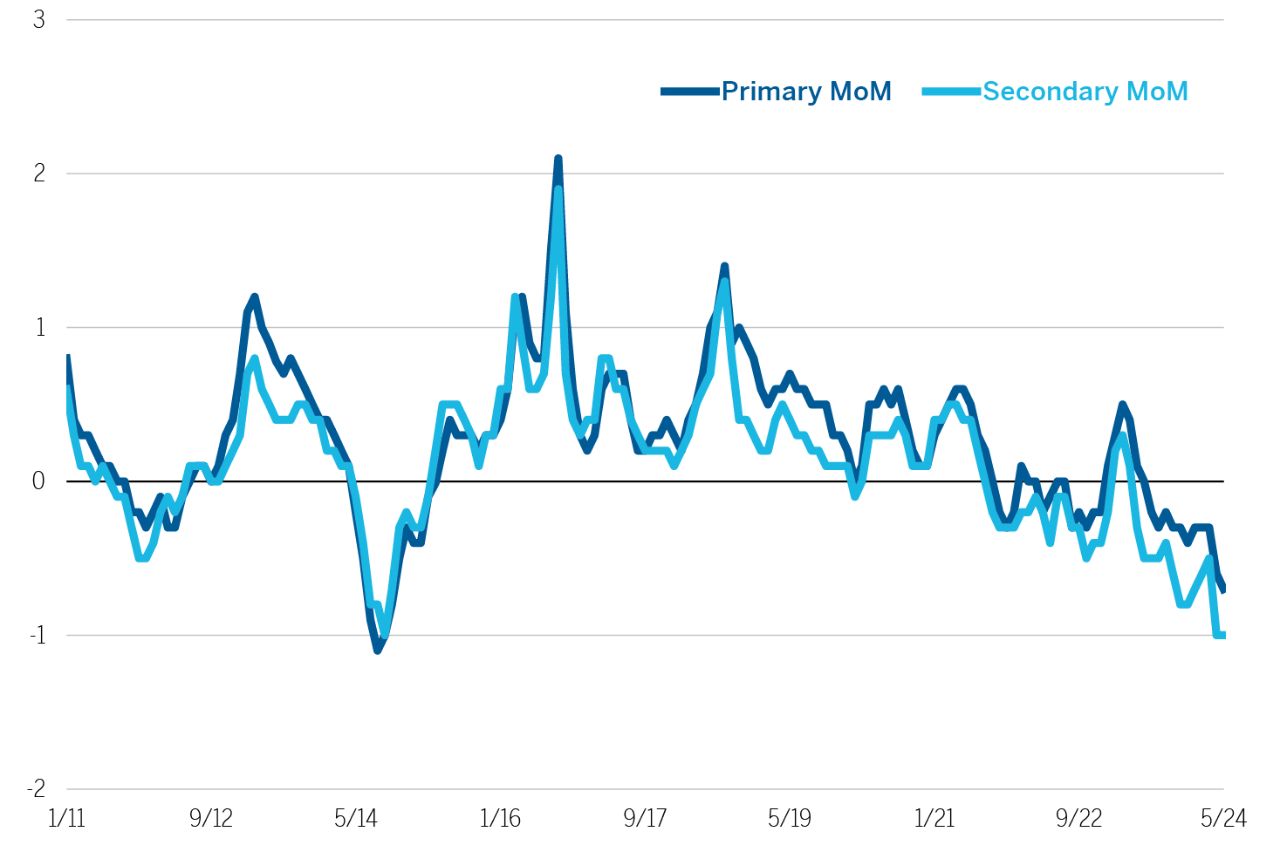

We’ve raised our view on China and EMs broadly to neutral, thanks in part to the beginning of a rate-cutting cycle, albeit one that’s likely to be shallow. We’re also less willing to maintain an underweight view on China given cheap valuations, which recently drove a sharp rally. At the same time, structural headwinds and the lack of policy traction (FIGURE 1) keep us on the sidelines and reluctant to engage positively.