If recessions aren’t the primary driver of value/growth cycles, what is? To answer that, we looked at a broad pool of style factors to identify those with the highest and most stable explanatory power (R-squared)3 for value/growth performance. We also interviewed a range of Wellington value and growth portfolio managers about their investment process, to help confirm our quantitative findings.

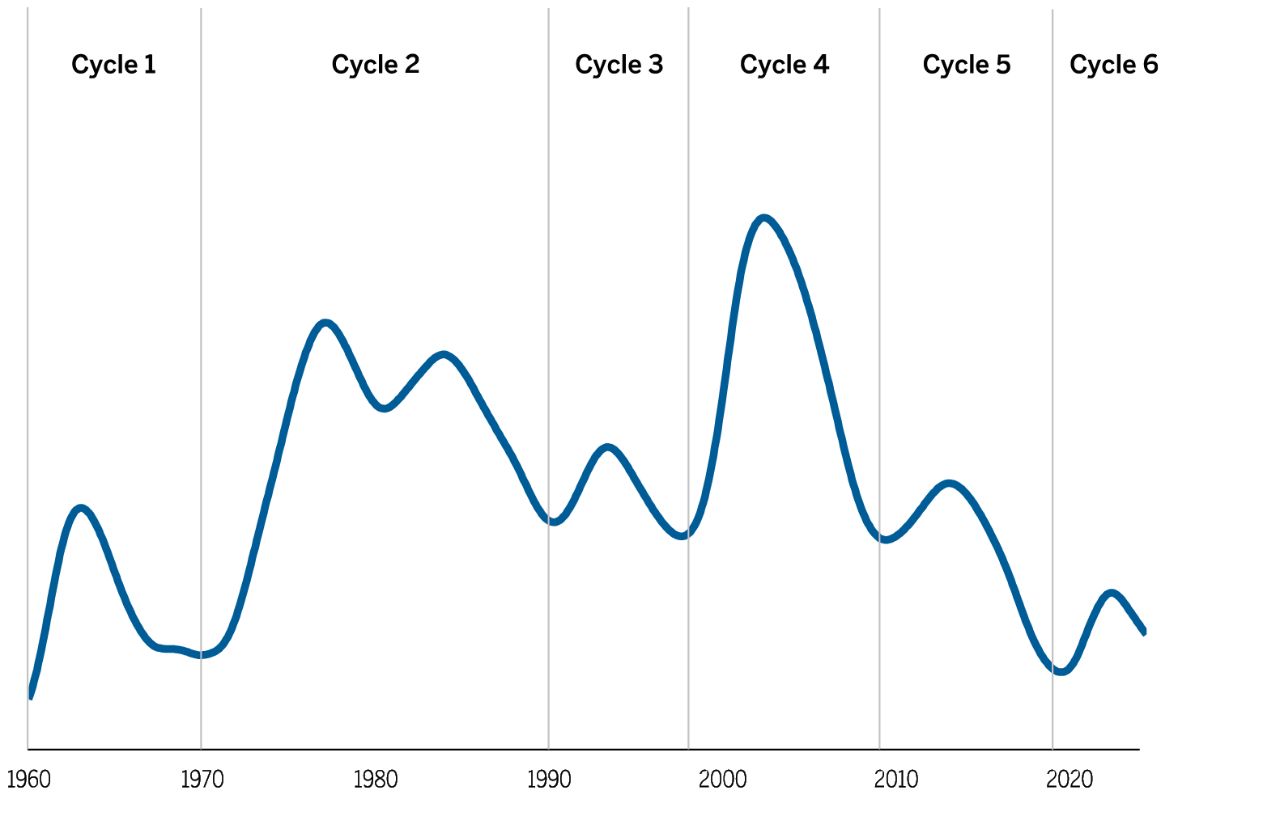

Our analysis revealed that three factors have tended to drive value outperformance: higher inflation, higher real interest rates, and higher economic growth (real GDP). Importantly, the impact of these drivers can vary greatly from one regime to another. Consider some of the stronger periods for value. During the 1970s, for example, high inflation played a significant role in value’s outperformance. The first half of the 1990s was a period of strong economic growth coming out of the US savings-and-loan crisis. The post dot-com bubble years (2000–2005) were another positive period for value, powered by elevated real rates and relatively solid growth.

Turning to the weaker periods, value barely broke into positive territory during the first half of the 1960s thanks to mediocre growth, record low inflation, and real interest rates close to zero. Value struggled from a similar mix of factors during the period following the Great Financial Crisis, from 2010–2020. Since the COVID-19 pandemic, value has been held back primarily by recession fears and artificial-intelligence (AI) enthusiasm.

Sector Diversification: Value Has Come a Long Way

Another common assumption is that value stocks are generally limited to mature, cyclical sectors, such as financials, energy, materials, and industrials—all of which are often characterized by low price-earnings (P/E) ratios,4 stable cash flows, low growth rates, and high-dividend yields. Conversely, growth stocks are typically linked to sectors that are considered innovative or disruptive and have higher P/E ratios, such as technology, healthcare, and consumer discretionary.

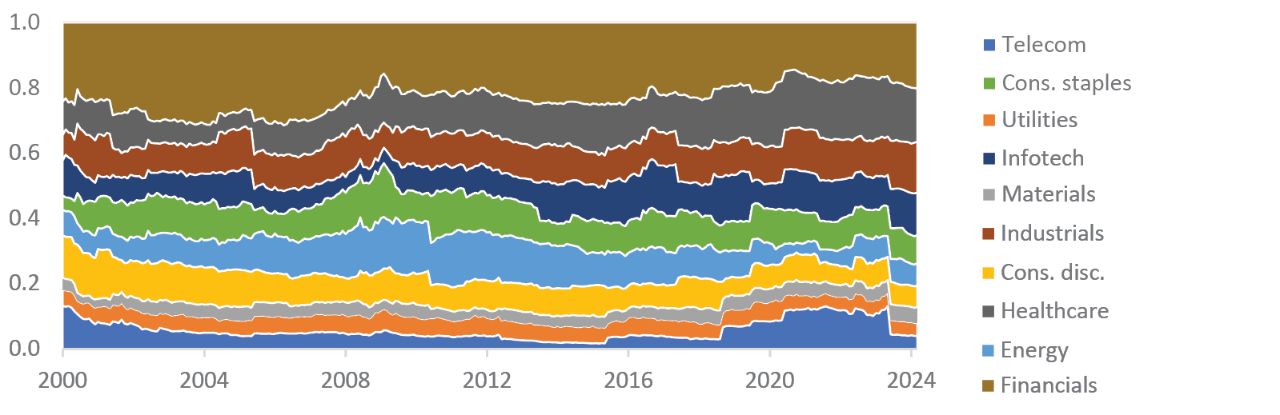

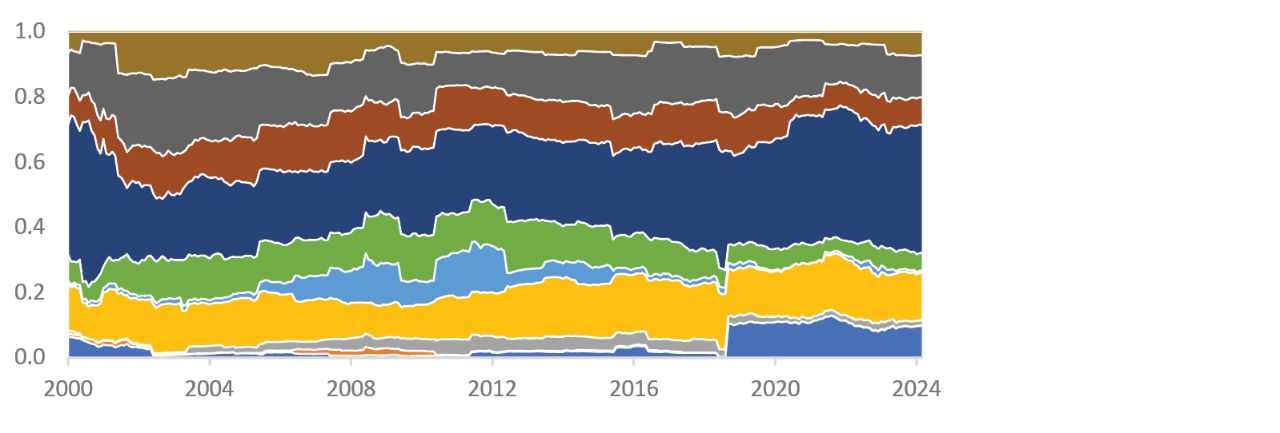

We found that over time the sector composition of the value and growth stock universes has changed markedly. As shown in the top chart in FIGURE 3, value has become less concentrated and more diversified than growth, as the latter has been reshaped by the growth of megacap stocks in the IT, communications, and consumer discretionary sectors. (It should be noted that there have been times when some of these same stocks have been designated as “value,” due to their low price-book ratios,5 and that index rules that govern value/growth designations vary.)

Currently, value’s largest weights are in healthcare (16%) and financials (20%), followed by industrials (15%), IT (13%), and consumer staples (9%). Energy is only at 7%. This is a very different mix than 10 years ago, when energy and financials made up 13% and 25% of the value index, respectively. The large weight of IT in the value index may be especially surprising to some; it's driven by industries such as hardware, semiconductors, IT services, and communications equipment, rather than software companies, which are more likely to be found in the growth index. As shown in the bottom chart in FIGURE 3, growth is highly concentrated in IT (almost 40%, up from 25% a decade ago), followed by healthcare and consumer discretionary at about 15% each.

Sector changes like those we’ve described tend to occur over long periods of time, so we expect value to continue providing more sector diversification than growth for the foreseeable future.