Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

When it comes to planning for a financially secure retirement, starting early can make all the difference. While retirement savings may seem like a concern for adulthood, putting away even a small amount from a summer job can help get savings off to a strong start. One smart option is a Roth IRA, a type of individual retirement account designed to help people save and invest for the future. These accounts allow individuals to contribute money they’ve already paid taxes on, with the potential to grow over time and be withdrawn tax-free in retirement—making them especially appealing for young savers.

The Power of Compounding

By starting early, young investors give their portfolios more time to benefit from the power of compounding. For example, contributing $3,500 annually from ages 16 to 21 can potentially lead to significant growth over time, thanks to the extended period those investments have to accumulate returns.

FIGURE 1

Contributing Early to a Roth IRA Can Lead to Significant Growth Over Time

Hypothetical $3,500 Contribution From Ages 16 to 21

| Age | Annual Contribution |

Total Contribution |

Estimated Value (8% Annually) |

|---|---|---|---|

| 16 | $3,500 | $3,500 | $3,780 |

| 17 | $3,500 | $7,000 | $7,862 |

| 18 | $3,500 | $10,500 | $12,271 |

| 19 | $3,500 | $14,000 | $17,033 |

| 20 | $3,500 | $17,500 | $22,176 |

| 21 | $3,500 | $21,000 | $27,730 |

| 68 | - | $21,000 | $1,032,437 |

The compounding example is a hypothetical example that assumes a $3,500 annual contribution and annual 8% return. Also assumes that an investor stays below the 2025 income limitations to contribute to a Roth IRA which are less than $150,000 for full eligibility for single filers and less than $236,000 for full eligibility for married filers. The example doesn’t represent any particular investment and is for illustrative purposes only to show the mathematical concept of compounding. It does not account for inflation, and the rate is not guaranteed. Taxes are not included in the calculations. Investments are subject to risk, including the loss of principal.

Maximizing Earnings From Summer Jobs

At first glance, contributing $3,500 annually at a young age might seem out of reach—but with a typical summer job, it can be surprisingly attainable. With an average hourly rate of $16 for teens in 2024,1 working 40 hours per week for 12 weeks would yield $7,680 before taxes. The IRS allows contributions of up to $7,000 in earned income, making it feasible to set aside a significant portion of summer earnings.

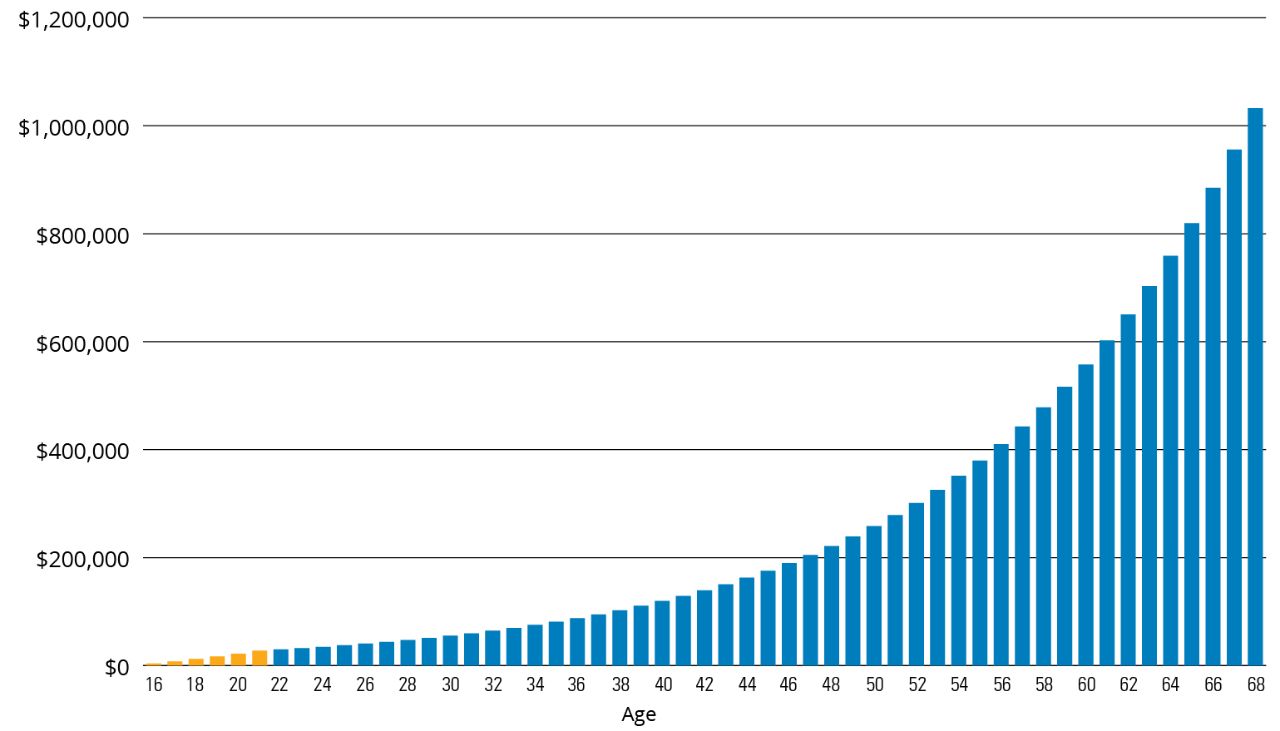

FIGURE 2 shows how consistent and early annual contributions of $3,500 to a Roth IRA from ages 16 to 21 could significantly grow a retirement fund by age 68.

FIGURE 1

Compounding Can Grow Small Contributions Into a Sizable Nest Egg

Hypothetical $3,500 Contribution From Ages 16 to 21 With 8% Returns Until Age 68

The compounding example is a hypothetical example that assumes a $3,500 annual contribution and annual 8% return. Also assumes that an investor stays below the 2025 income limitations to contribute to a Roth IRA which are less than $150,000 for full eligibility for single filers and less than $236,000 for full eligibility for married filers. The example doesn’t represent any particular investment and is for illustrative purposes only to show the mathematical concept of compounding. It does not account for inflation, and the rate is not guaranteed. Taxes are not included in the calculations. Investments are subject to risk, including the loss of principal.

Offering matching or gifted contributions can help teens stay motivated and work toward specific savings milestones.

Parents Can Help

Parents play a pivotal role in shaping their teen’s financial future—not just by contributing funds, but by modeling smart financial behavior and fostering a mindset of long-term planning. Offering matching or gifted contributions can help teens stay motivated and work toward specific savings milestones. These early contributions, paired with encouragement, can help teens feel that their financial goals are both real and reachable.

While parents are allowed to contribute to a teen’s Roth IRA, it’s crucial to note that the amount parents contribute is still subject to the child’s earned income that they declare to the IRS. IRS rules don’t specify where contributions come from as long as they don’t exceed the child’s earned income for the year.

Beyond dollars, parents can use this opportunity to teach essential financial concepts such as budgeting, compound interest, and the importance of delayed gratification. Discussing investment choices together, reviewing account statements, and setting shared milestones can turn saving into a collaborative learning experience.

Benefits of a Roth IRA

One of the main advantages of a Roth IRA is the ability to withdraw funds tax-free in retirement. For young investors, who are likely in a very low or zero tax bracket, this means investing for retirement now can have a beneficial tax impact later.

Contributions to a Roth IRA can be withdrawn at any time tax-free and penalty-free, though the earnings on those contributions may be subject to a 10% penalty and subject of income taxes under most circumstances. For a withdrawal to be completely tax-free, the account must have been open for at least five years, and the account holder must meet one of the following conditions: reaching age 59½ or older, becoming disabled, using the funds for a first-time home purchase (up to a $10,000 lifetime limit), or the withdrawal being made by a beneficiary after the account holder’s death.

Instilling Good Financial Habits

Early and consistent investing in a Roth IRA helps encourage good saving habits in young people while also growing their retirement funds. Starting during teenage years provides ample time to develop these crucial habits and can help put young investors on a path to financial independence.

Just as importantly, investing early gives money more time to grow. Thanks to the power of compounding, even small contributions made in the teen years can potentially grow into a sizable nest egg over decades. This combination of habit-building and long-term financial growth makes early investing one of the most impactful steps a young person can take toward a secure future and a more comfortable retirement.

For more information on investing in a Roth IRA, talk to a financial professional.

1 CNBC, “‘The Summer Job Is Back’: Teens Enter the Labor Force As Employers Dish Out Higher Wages, Perks” 8/4/24. Most recent data available.

Important Risks: Investing involves risk, including the possible loss of principal.

Investment options offered through IRA providers vary and any fees and expenses will differ.

A Roth IRA is a retirement savings account funded with after-tax income. Although contributions are not tax-deductible, the investments within the account grow tax-free. Qualified withdrawals made during retirement are also tax-free, provided certain conditions are met. This structure allows taxes to be paid upfront, with no tax owed on earnings or withdrawals later.

This information should not be considered investment advice or a recommendation to buy/sell any security or tax advice. In addition, it does not take into account the specific investment objectives, tax, and financial condition of any specific person. Investors should consult with their own financial professional for additional information.

This information is written in connection with the promotion or marketing of the matter(s) addressed in this material. The information cannot be used or relied upon for the purpose of avoiding IRS penalties.

This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. This material and/or its contents are current at the time of writing and are subject to change without notice.